Most people think the cost of insurance is the premium.

That is understandable for a variety of reasons. Two of those reasons are that most insurance salespersons and many insurance companies stress buying your insurance based on premium. That creates a huge problem because:

Premium is not the true cost of your insurance program.

The true cost can only be calculated when you actually use the policy after an accident or claim. At that point, the cost is not just the premium. It is the total of three numbers:

Premium + Deductible + Losses You Pay Out of Your Own Pocket

That third number is often the most important one.

If your coverage limits are adequate, your total cost will be limited to the insurance premium and the deductible. But if your coverage is not adequate, the amount you personally pay can become financially serious. That is where focusing only on price can create a dangerous vulnerability.

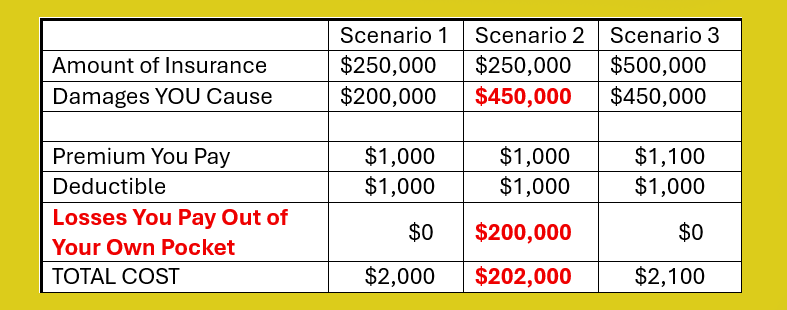

Consider the following simplified example.

In the first scenario, you have $250,000 of coverage and you caused $200,000 of damages. This coverage level is adequate for the severity created by this particular accident . Your total cost is the premium plus the deductible, or $2,000.

That is what most people expect when they buy insurance.

In the second scenario, you still have $250,000 of coverage, but you caused $450,000 of damages. The coverage is no longer enough because of the severity of the accident. The damages exceeded the policy limit by $200,000. That amount will likely become your personal responsibility.

Now the true cost of the insurance program is not $2,000. It is $202,000.

Note: Accident severity addresses the question “How much damage can I cause”. It’s sometimes thought of as a worse case scenario but it may not be. For example, medical bills and loss of a person’s ability to earn a living are driving the potential severity of an accident skyward.

So, the hidden danger is focusing only on premium. The policy may look affordable until the loss exceeds the protection.

In the third scenario, the vulnerability is addressed before the accident occurs. The coverage is increased from $250,000 to $500,000 with an additional $100 of premium. The damages are still $450,000, but the policy limit is now high enough to respond. In this scenario, you only pay the premium and deductible, for a total of $2,100.

To drive this point home, in scenario 3, we used the leveraged advantage of insurance to purchase an additional $250,000 of coverage and the premium was only $100. This helped avoid a potential $200,000 out-of-pocket exposure.

That is risk management.

Another very important point is that every person needs coverage limits that are based on the potential severity of a loss, their assets, income, lifestyle, and future financial exposure etc. Everyone must also understand that potential loss severity scenarios continue to change rapidly. That is another discussion.

One of the most important things an insurance advisor can do is to help you identify risks and vulnerabilities BEFORE a claim occurs and recommend practical ways to reduce those vulnerabilities.

You should NOT be paying an agent to just provide a quote. You SHOULD be paying an agent to help you identify risks, understand consequences, and make better protection decisions.

THE LOWEST PREMIUM IS USUALLY NOT THE LOWEST COST.

THE TRUE COST IS ONLY REVEALED AFTER THE ACCIDENT!!

That brings up the subject of “Probability” or “What are my chances of being involved in a bad accident”? We’ll discuss that in another article.

Email me and we can talk. Contact US

Comments are closed