It is recommended that you read the blog posting titled “Why I need to MANAGE the RISKS in My Life” and “How can I use Insurance to help me Manage Risks” before you read this blog.

When most consumers are asked this question “What is the REAL cost of your insurance policy”, many will have a puzzled look and most will respond, “It’s my insurance premium” or something similar.

The REAL cost we should be looking at is the cost of your Risk Management Program. Insurance is just one of the costs that contribute to the total cost of our Risk Management Costs. The only time we can accurately determine how much our insurance policy costs us is when we use it. When we have a claim. Then we add up the following three numbers.

- Your Insurance Premium

- Your Deductible

- The Losses You Must Pay out of Your own pocket.

Most consumers ASSUME that their insurance policy will pay for ANY and ALL accidents in which they are involved. Particularly if they have “Full Coverage.” THAT IS NOT THE CASE. This is particularly true of your Liability coverages. Your insurance policy will only pay UP TO the amount of money shown on the policy declarations page. YOU must pay for any losses or judgments which exceed that amount. Let’s look at a simple example:

Note: Some exceptions to this are your comprehensive and collision coverages.

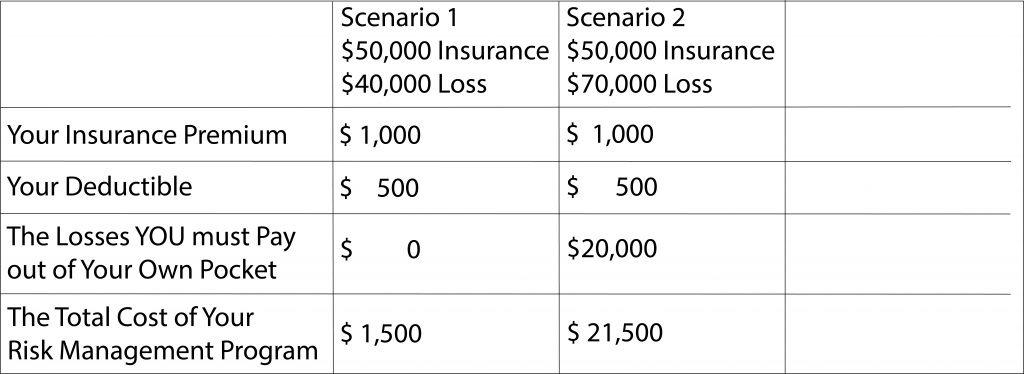

Lets assume you have liability limits of $50,000 and that you cause a $40,000 accident. (Note: A $40,000 claim is not a very large claim anymore.) Since the $40,000 claim is less than the amount of insurance you have, the insurance company will pay the entire $40,000 loss. So the Losses You Must Pay out of your own pocket are Zero. If you have a $500 collision deductible, the cost of your Risk Management Program would look like this:

No surprises. Now lets change the scenario a little. Instead of causing a $40,000 accident, the damages come out to be $70,000 with the same liability limits and the same deductible. Your program costs for Scenario 2 would like this.

Since the $70,000 loss exceeds your $50,000 liability coverage, the extra $20,000 comes out of YOUR pocket. You may have to withdraw money from your savings, take a 2nd mortgage on your home, dip into your 401k etc. to pay for this judgement against you. (Also, this judgement could reduce your credit score which will cause other problems.) This is not a good way to manage risks.

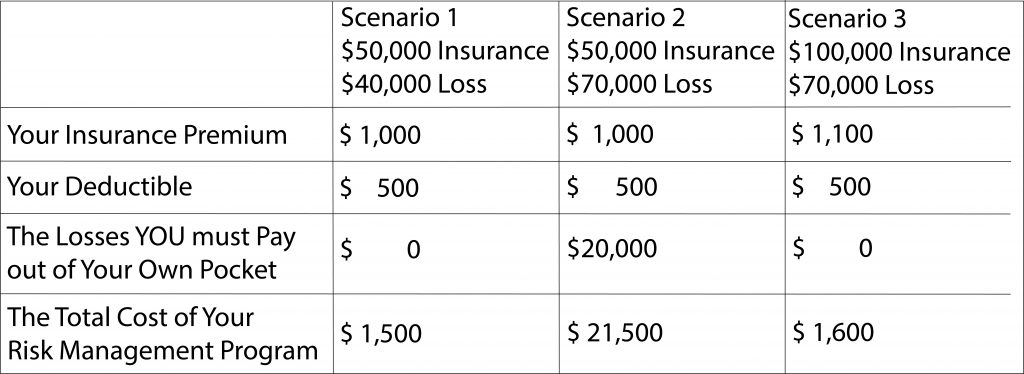

Lets consider a third scenario which helps you solve this problem. So you decide to increase your liability limits to $100,000 to protect your assets. Let’s assume the increased liability limits cost you $100. Now, if you have that same $70,000 loss the numbers might look like this.

It doesn’t take a rocket scientist to figure out which “Total Cost” you want to pay out of the three scenarios. You also note that the big numbers are in the Losses You Must Pay out of your own pocket line, not on the premium line.

Note: This pattern could go on and on. Thankfully there are some good Risk Management principles that can be applied to figure out how much coverage you need to protect what you have so this cycle does not go on forever.

There are a couple of important things we can learn from these scenarios.

- A small amount of extra premium dramatically increases the amount of coverage you are able to purchase. $100 purchased an additional $50,000 of liability coverage. So, it does not take much money to get the coverage you need to protect what you have. This is where you leverage your money. (Note: these numbers are just examples and your numbers will probably be different. We actually need to do a review to find that out.)

- The big money is not in the premium. It is in the Losses you Must Pay out of Your own Pocket when your coverages are not adequate. What you are paying your agent to do is to identify those types of losses. And then help you design a Risk Management Program which gets rid of those losses. To make them go away. To make them zero. Unfortunately, an Apples to Apples quote will not reveal this problem.

About 70% of the policies we review would not protect the family if they were involved in a serious accident.

Agents who just ask you “What coverages you have” to give you an Apples to Apples quote are not doing you any favors. Your agent needs to spend some time helping you make sure you have the coverage you need.

We should spend a little time together to review your account to make sure you don’t have this or a similar situation. If you do, we can help you create a program which has a higher probability of protecting your family and your assets. And we can probably SAVE you some money on your premium in the process.

Contact Us today to get a Quote or to Start a Discussion

Call us at 419-874-8055 or

Email us at rhamilton@fireflyagency.com or

Contact us by filling out the Contact Form below.

Comments are closed